In 2019, only 1 of the top 20 blockchains by market capitalization was a Proof of Stake blockchain (Tezos), with a total value staked of around $50 million. Today, 16 of the top 20 blockchains are Proof of Stake (excl. Bitcoin, Dogecoin, Bitcoin Classic, and Litecoin), with a total market cap of around $850 billion; representing about 22% of the total market cap of all cryptocurrencies. Without BTC, PoS would represent 50%. If this trend is to continue, staking will serve an increasingly important role in both securing blockchains and delivering value to market participants.

2024 has also seen the global acceleration of publicly traded crypto ETFs, with Bitcoin and Ethereum ETFs notably receiving approval from the U.S. SEC. As a Proof of Stake blockchain, Ethereum can offer unique value to ETF issuers and holders, but also poses new regulatory hurdles, and operational and risk considerations.

What considerations should you take when staking ETH?

There is clear market demand for ETH on its own, but with staking as a native mechanism to secure the Ethereum blockchain while simultaneously rewarding stakers with yield, any ETH investment product that does not include staking is likely falling short. Today in the U.S., there are many ETH ETFs, but none of them include staking due to the SEC pushing back on all ETH ETF S-1s that initially proposed staking. This is not the case in other jurisdictions; Switzerland, Canada, and others have approved staking for the underlying ETH, primarily for investors who, in some form, can increase their returns through ETH staking rewards. Issuers can earn a spread on total staking rewards, and investors can see returns in the form of, for example, increased NAV (and therefore share price), reduced management fees, and even dividends.

ETFs offer the path of least resistance for institutional funds who want to participate in the ecosystem. Purchasing spot and staking may be more lucrative, but will likely require more upfront work and costs. If a fund wants to purchase spot ETH and stake, this could open a can of worms: self custody vs. qualified custody, running your own validator vs. evaluating third party offerings, commercial negotiations, legal agreements, procurement, risk considerations, and more. Any fund who wants ETH exposure and is deciding between the two options will likely consider:

- Returns: How much can I earn from an ETF vs. purchasing spot and staking? Do the ETFs in my region include staking?

- Costs: What are the management fees vs. infrastructure costs?

- Regulatory Requirements: Will my regulator let me stake?

- Operations: Is it worth the effort to run our own infrastructure and reconcile rewards?

- Risks and Control: Given risks around slashing, do we want to hand-pick our staking product stack and partners or rely on a pre-built stack from an ETF issuer? Can we get more comfortable with the risks if we control all aspects of the stack and thereby earn more rewards? Are there standards or tools to make diligence for validator operators more efficient?

As more and more investors become comfortable (and eager) to have ETH exposure, these considerations should help investors decide which route is best for them.

Ethereum’s technical evolution: smart contracts, the merge, and staking mechanics

Ethereum launched in 2015 with smart contracts as its key innovation. Smart contracts enable computer programs (and therefore, business logic) to be executed and enforced, while leveraging blockchain to remove the need for a centralized 3rd party to enforce these programs. Ethereum was initially launched as a Proof of Work blockchain, similar to Bitcoin, with the intention to eventually transition to a Proof of Stake blockchain. This was set in motion with a few key milestones: in 2017, “Ethereum 2.0” was introduced, in 2020 the “Beacon Chain” was launched, and finally in 2022, Ethereum merged with the Beacon Chain to finalize Ethereum’s transition from a Proof of Work blockchain to a Proof of Stake blockchain.

Proof of Stake relies on ‘stakers’ who lock up their ETH as they validate blocks, thereby securing the blockchain. Good actors who do this properly are rewarded in native yield, while bad actors who submit incorrect data can be penalized and have their locked ETH slashed. For investors who are long on ETH, this means that in addition to ETH price appreciation, you can also stake to earn yield denominated in ETH, which currently averages around 3-4% APY.

The road to the current ETF market

In the US, spot crypto ETFs have been a narrative for nearly as long as Bitcoin has been around. Private Bitcoin funds have been around since as early as 2013 with the launch of Grayscale’s Bitcoin Trust, which was initially made available to certain accredited investors. Over time, these products have gone through iterations from private funds, to public quotations (private allocations that can be sold on the secondary market to non-accredited investors), and finally to a true public listing, where creation redemption mechanisms incentivize for the ETF price to stay roughly pegged to the value of the underlying asset.

After the SEC approved the first few Bitcoin ETFs in January 2024, Ethereum ETFs were quick to follow with approvals in May 2024. Staking was not a consideration for the Bitcoin ETFs as Bitcoin is famously a Proof of Work blockchain, where the Bitcoin consensus mechanism relies on computational work. Conversely, staking is a key consideration for the Ethereum ETFs, as staking is a core feature of Ethereum. Many of the Ethereum ETF S-1 submissions initially contained staking, but were updated to remove staking in the days leading up to the SEC’s approval of the Ethereum ETFs. It can be assumed that the SEC implied the ETFs would only be approved if the Ethereum ETFs did not include staking.

Staking is already included in many publicly traded structured products outside of the United States. For instance, investors can gain exposure to both ETH price appreciation and staking rewards through VanEck’s Ethereum ETF (VETH), which is traded on European exchanges including Deutsche Borse, SIX Swiss Exchange, and Euronext. Based on the trends of US regulatory approvals, institutional adoption of cryptocurrencies, staking ETFs approved outside of the US, and an anticipated change in SEC leadership, many issuers and investors are anticipating that staking will eventually be approved for Ethereum ETFs in the US.

How does a ‘crypto ETF’ work under the hood?

A few important terms in the context of an exchange traded product:

- Net Asset Value (NAV): the actual value per share of an ETF (assets – liabilities / number of shares)

- Market Price: the cost to purchase a share of an ETF on the open market

- Arbitrageur: a market participant who looks for price inefficiencies, or different prices of the same asset, e.g. Market Price vs. NAV per share

- Qualified Custodian (QC): a market participant who is licensed by regulators to “custody,” or hold, certain assets on behalf of others

- Authorized Participant (AP): a market participant who can offer creation and redemption between spot ETH and the ETF shares

- Benchmark Index: a reference rate for an asset, in this case ETH, for issuers to use in NAV calculations

Exchange Traded Products or Funds can enable investors to have price exposure to an ETF’s underlying asset (in this case, ETH) without having to purchase spot ETH, which may have additional risks and operational considerations like key management and self custody, or counterparty risk. In the US, ETFs may have other trade offs vs. spot ETH like SPIC insurance, or it can be easier for large regulated funds like pension funds to participate in exchange for a management fee.

ETF issuers will leverage Qualified Custodians to securely custody the underlying cryptocurrencies, and will assign Authorized Participants to create or redeem shares of the ETF. Creation is the creation of an ETF share based on the deposit of the asset(s) that the share represents, and Redemption is the redemption of the ETF share for the underlying assets that it represents. This mechanism enables arbitrageurs to profit when there is a price mismatch, thereby keeping the market efficient, or keeping the NAV and market price as close as possible. NAV is determined by leveraging Benchmark Indices, which set a benchmark rate or price for the underlying asset based on trading activity across exchanges.

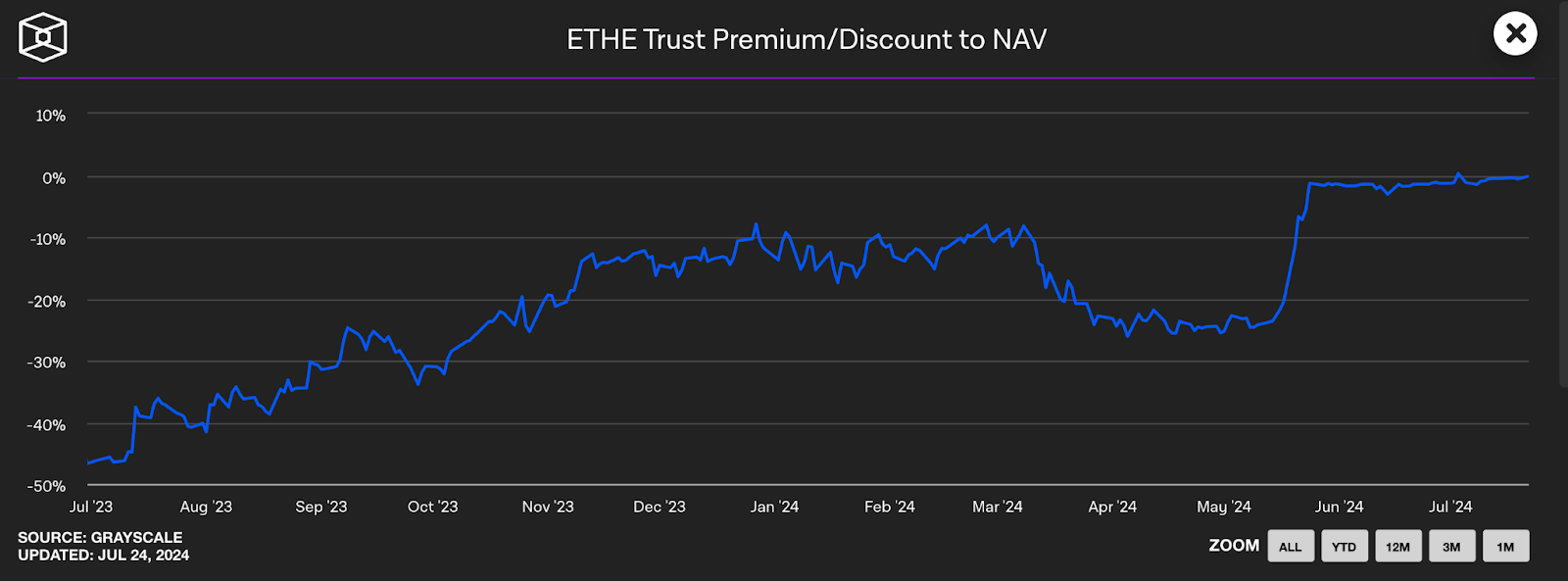

When ETH structured funds were still private, prior to being approved for public listing, and therefore before APs were able to offer creation and redemption, there was often a significant mismatch between market price and NAV. ETHE for example traded at a significant discount to NAV, which many investors including Jonah Van Bourg and Avi Felman on the 1000x Podcast highlighted as a potential opportunity where public listing would close the discount to NAV. If an investor were to purchase ETHE in July 2023 at a ~50% discount to NAV, as long as ETHE eventually converted to a publicly traded ETF, investors would enjoy 50% appreciation of the share price as it returned to NAV plus any additional appreciation of the underlying ETH.

Discount to NAV was nearly 50% in July 2023, but slowly converged to 0% as investor confidence grew in ETHE being publicly listed. ETHE now trades close to NAV. For example as of Dec 5, 2024, ETHE NAV was $32.18 while Market Price was $32.14, for a very slight discount of -0.12%. Sources: The Block, Grayscale

Staking yields and ETF strategies

In the US as of Dec. 1, 2024, ETFs currently do not include staking. Prominent Ethereum staking indices like the MarketVector™ Figment Ethereum Staking Reward Reference Rate (STKR), and CESR™ which is administered by CoinFund and calculated by CoinDesk Indices, show a Dec. 5, 2024 close of 3.48% and 3.22% respectively. Staking can offer significant returns to investors on what many consider to be a relatively low-risk activity. Some non-US ETF models like 21Shares’ Ethereum Staking ETF, AETH, offer this staking yield in the form of NAV accrual, where the underlying assets increase in value over time. Others like CoinShares’ Physical Ethereum Staked ETF, ETHE, may offer smaller increase in NAV than 21Shares (1.25% vs. 21Shares’ 1.65%), but may also offer lower management fees (0% vs 21Shares’ 1.49%)8. There may be more models to emerge over time, including even potentially paying out ETH staking yield to investors in the form of a dividend.

The total percent of ETH staked will also impact staking rewards for ETF holders. ETH staking inherently involves locking ETH for a period of time to validate blocks – with total unstaking time in the range of a few days or weeks, issuers need to ensure liquidity given they are required to process any redemptions within 24 hours. Given the limitations on liquidity most ETFs are not staking all of ETH within their products. VanEck, for example, currently has ~65% of the ETH in VETH staked. Looking forward, liquidity solutions like Liquid Staking Tokens (LSTs) may offer solutions to this, where ETH depositors can mint liquid tokens representing their staked ETH. With sufficient market liquidity, these tokens may serve as a viable option for issuers to increase total ETH staked and therefore pass more yield on to investors. Lido stETH is currently the largest ETH LST with a market capitalization of $39 billion and 28% of total staked ETH market share – stETH, along with other institutional focused LSTs like The Liquid Collective’s LsETH, may be preferred options for issuers.

Current state of ETH ETF market

The following table includes a few prominent ETF issuers and their associated products and jurisdictions, but does not include or represent the entire market:

| ETF Issuer | Ticker | Staking | Registered | Exchanges |

| Grayscale | ETHE | No | US | NYSE |

| 21Shares | AETH | Yes | CH, DE, UK, more | SIX, Deutsche Borse, Euronext, LSE |

| CoinShares | ETHE | Yes | CH, DE, more | SIX, Euronext |

| Purpose Investments | ETHC.B | Yes | Canada | Cboe Canada |

| VanEck Ethereum ETN | VETH | Yes | CH, DE, FR, more | SIX, Deutsche Borse, Euronext |

| ChinaAMC Ether ETF | 3046 HK | No | Hong Kong | HKEX |

| ProShares Ether ETF | EETH | No* | US | NYSE |

*EETH invests in ether futures and does not invest directly in ether

For investors who want exposure to ETH and associated staking rewards, staking spot ETH or purchasing an ETH staking ETP are both viable options. Investors must weigh potential returns, costs, regulatory requirements, operational preferences, and risks when making this decision. For many institutional investors, an ETH ETP may offer the path of least resistance to quickly get to value with minimal upfront investment. Investors who are comfortable staking spot ETH may realize higher returns and have the ability to customize and optimize their tech stack.

As the leading institutional platform for secure digital asset management and operations, Fireblocks enables customers to securely manage the ETH staking lifecycle with the optionality to use their preferred ETH validators.

Fireblocks is an easy-to-use platform to create new blockchain-based products, and manage day-to-day digital asset operations. Exchanges, banks, PSPs, lending desks, custodians, trading desks, and hedge funds can securely scale their digital asset operations through the Fireblocks Network and MPC-based Wallet Infrastructure.

Fireblocks serves thousands of organizations in the financial, payments, and web3 space, has secured the transfer of over $6 trillion in digital assets and has a unique insurance policy that covers assets in storage and transit. Head here to learn more.