The financial system at large has experienced a paradigm shift in the past year. A high-level transition to a digital economy is well underway, with the world’s top financial players increasing their investment in diverse areas from Bitcoin to DeFi to CBDCs.

On Mar. 29th, Visa announced that they will allow their users to utilize cryptocurrency (specifically USDC) on their payment network – joining the likes of BNY Mellon, Mastercard, and BlackRock Inc., who have all signaled their acceptance of digital assets as a major element of their financial strategy for years to come.

With another top institution announcing their investment in crypto each and every day, we have reached a boiling point for banks to embrace digital assets. As FIs across the world begin to launch products and services in this space, it’s becoming clear that those banks who are unable to adapt may have to face the consequences in the long term.

These are some of the main developments that are encouraging more and more banks to explore digital assets in earnest:

Digital wallets are overtaking their traditional counterparts

According to research by ARK Invest, digital wallets represent a $4.6 trillion opportunity and could replace physical bank branches if traditional financial institutions can’t adapt.

In China, mobile payments have multiplied more than 15-fold in just five years, from roughly $2 trillion in 2015 to an estimated $36 trillion. Meanwhile, in the US, digital wallet users are surpassing the number of deposit account holders at the largest financial institutions. At the end of 2020, the number of J.P. Morgan Chase deposit account holders totaled approximately 60 million, while Cash App’s and Venmo’s Annual Active Users (AAUs) scaled to 59 million and 69 million respectively.

It appears that digital wallets could entirely replace their traditional counterparts if banks can’t keep up with the digitization of the full financial services stack. Digital-native institutions like PayPal and Square are already offering digital asset services; today, many consumers are looking to use wallets that allow them to spend crypto just as easily as they spend fiat.

In order to power a new generation of digital products and services and compete with these digital counterparts, banks need to explore crypto and blockchain technology – from custody services to stablecoins and beyond.

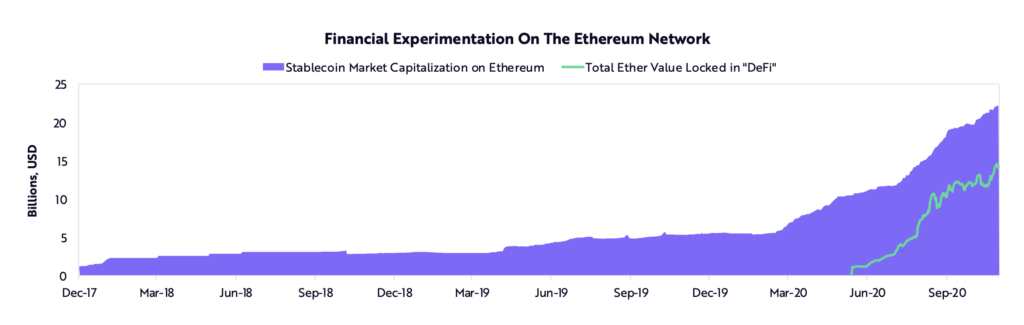

DeFi continues to gain traction

The explosion of decentralized finance (“DeFi”) has been a large factor in digital assets’ growing mainstream popularity. DeFi lets market participants cut out the need for middlemen and directly access financial services like credit & lending, market making, trading, and investing.

Today, there’s $44 billion total value locked in DeFi and top influencers like Elon Musk are endorsing the decentralized finance ecosystem.

People are looking to reap the benefits of services like crypto yield farming, high-yield savings accounts, and staking. Without having a secure channel to access crypto through financial institutions, they’re utilizing DeFi protocols to do so. While many investors would likely prefer to use their banks to access these services, more and more are learning about and investing in DeFi in the absence of other options.

This chart from ARK Invest demonstrates DeFi’s massive growth over the last year.

To stay competitive as DeFi explodes, banks need to better understand and prepare for these types of digital asset services.

Regulations have blossomed across the globe

Across the world, new regulations around digital assets are continuing to improve clarity. This is enabling institutions to enter the space in earnest.

The UK recently announced that they will create crypto regulations around stablecoins. At the same time, new announcements from leading U.S. bank and securities regulators – like the Office of the Comptroller of the Currency (OCC) and the Securities and Exchange Commission (SEC) – are also giving organizations the go-ahead to provide their own digital asset custody solutions. Meanwhile, in the Asia-Pacific region, regulatory clarity also continues to increase, with new announcements around the regulation of exchanges in Hong Kong and the relationship between payments services and crypto assets in Singapore.

Essentially, regulators are getting out of the way for institutions, creating a clear path for investment in digital assets.

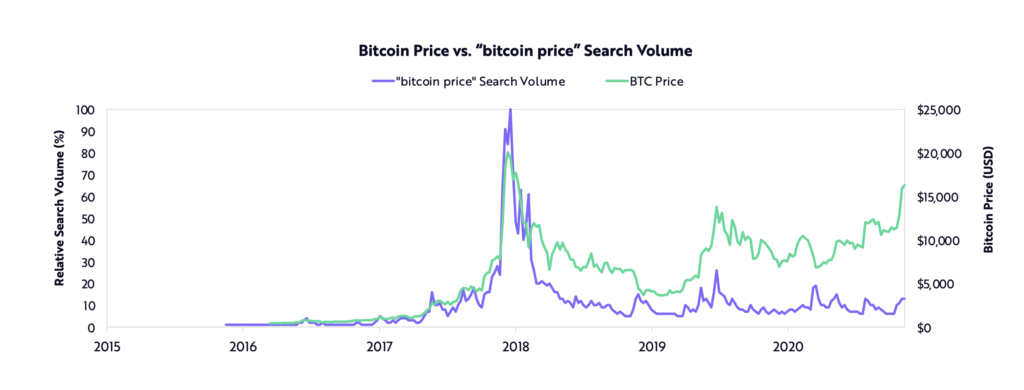

Institutional investors are seeing crypto as a hedge against fiat

Banks should also be aware that institutional investors are currently looking at crypto as a hedge against fiat, with some preparing to add it to their portfolio; many are already doing so.

One way to judge crypto’s state within the “hype cycle” is through comparing internet search volume for certain terms (e.g. “bitcoin”) with the actual price of a given digital asset. Based on search volumes compared to 2017, bitcoin’s recent explosion in price seems to be driven by more long-term factors, and less by hype. With bitcoin gaining more trust, institutions and companies are looking to add crypto as cash on their balance sheets.

Square and Microstrategy, both with balance sheet investments in bitcoin, are showing the way for public companies to deploy bitcoin as a legitimate alternative to cash. According to ARK Invest’s research, if all S&P 500 companies were to allocate 1% of their cash to bitcoin, its price could increase by approximately $40,000.

More institutional investors are planning to add crypto to their portfolios, and will first look to their banking partners to do so before looking for alternatives. It’s up to banks to make that a possibility.

What’s next for banks in the era of digitized finance?

These are just a few of the recent trends that point to our current moment being the boiling point for banks to enter the digital asset space. Many have already begun to do so – and those banks who can adapt to the new paradigm will reap the benefits in the years to come.

Fireblocks’ technology platform helps the largest players in the space develop various revenue models for digital assets, including:

- Digital asset custody and wallet management

- Tokenization

- Trading and prime brokerage

- Institutional and retail lending

- Payments solutions

Interested in learning more about how Fireblocks can help your organization explore the digital asset space? Download our latest whitepaper, Why Financial Institutions are Choosing to Custody Their Own Digital Assets or request access to speak with our team today.