On March 7, amid media focus on the first-ever White House Crypto Summit, the U.S.’s primary national bank regulator, the Office of the Comptroller of the Currency (OCC), quietly issued an interpretive letter that could have significant implications for how national banks engage with digital assets.

OCC Interpretive Letter 1183 (Addressing Certain Crypto-Asset Activities) signals a marked departure from the previous Administration’s stance on the legality of national banks’ engaging with digital assets. This letter provides clarity that banks have been waiting for—institutions now have additional certainty around what they can and cannot do.

Specifically, it reaffirms the first Trump Administration’s stance on permitting cryptocurrency custody, stablecoin networks, and certain operations related to payments. By removing supervisory pre-approvals—previously a major roadblock—the letter simplifies the process by which banks can start to engage with digital assets in a production environment.

However, these new permissible activities also introduce new risks for banks. Financial institutions, along with their supervisors, must now reassess their roadmaps to ensure they are prepared to address important issues—like digital asset security—that threaten the safety and soundness of institutions without well-designed and implemented risk management systems.

Models for what “good” looks like exist, such as those in place for institutions overseen by the New York Department of Financial Services (NYDFS), which specifically address crypto-related risks, vulnerabilities, and required controls. Yet even these models will need further tailoring and responsiveness to address novel activities, from digital asset custody and stablecoins to asset tokenization, which will increasingly operate within the regulatory perimeter. Institutions need to start assessing their plans, systems, and risk management frameworks now to stay ahead of this evolving landscape.

What are interpretive letters & how do they relate to cryptocurrency?

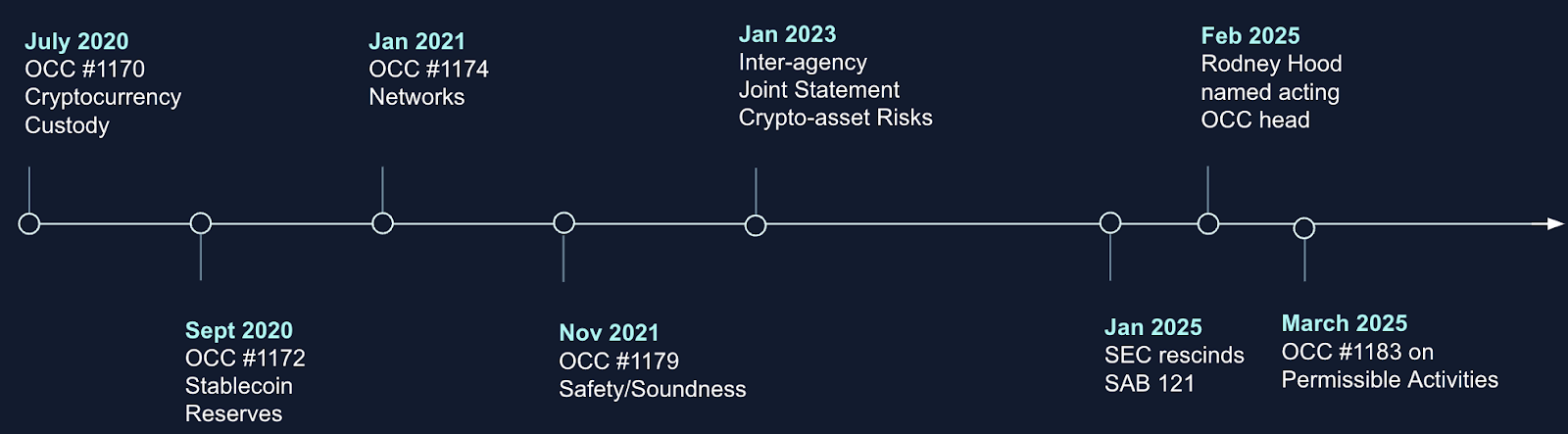

From July 2020 through January 2021, at the end of the first Trump Administration, we saw a range of interpretive letters that worked to engage directly with blockchain technologies and locate such business activity within the existing bank supervisory framework. At a high level, interpretive letters are a lot like what they sound like: they provide legal interpretations around permissibility for activities that national banks can partake in. Through these letters, the OCC documented how blockchain-related activity could be conducted, with appropriate guardrails. In sequence:

- #1170 provided clarity that, subject to an appropriate risk and compliance framework, banks were authorized to hold customer assets (including cryptocurrency) as part of their safekeeping and custodial services;

- #1172 allowed banks to hold deposits that served as reserves for stablecoins subject to appropriate considerations such as anti-money laundering and deposit insurance;

- #1174 addresses the permissibility of banks to engage with new technologies including “independent node verification networks” (e.g., distributed ledgers) and stablecoins to facilitate payments activities;

- #1179 introduced additional notification requirements and non-objection requirements by bank supervisory offices based on a bank’s risk management systems and controls; and

- #1183 rescinds #1179 explicitly (above), and reaffirms the prior letters (#1170, #1172, and #1174).

Timeline of OCC Interpretive Letters

Through the evolution depicted here, we can expect national banks to explore the types of activities laid out in prior letters, and consider product roadmaps that may extend further based on other permissible activities within this space, subject to appropriate risk management standards.

What next?

The OCC’s latest interpretive letter represents a pivotal moment in the evolving relationship between national banks and the cryptocurrency space. By reaffirming and expanding the scope of permissible crypto-related activities for banks, the letter signals that digital assets are no longer a niche area of financial innovation but a mainstream part of the banking landscape.

This is a critical shift—but it’s just the start. In our next blog, we’ll break down crypto-specific risks, unanswered questions, and what financial institutions need to prepare for next. And for more information on the current regulatory landscape, and the steps companies need to take to meet their regulatory obligations, read our latest white paper on navigating DORA here.